The Commission’s Auditing Division issues assessments for deficiencies of individual income tax, corporate franchise tax, sales tax, fuel tax and other tax types. Click here for detailed information about USTC audits.

Taxpayers often inquire about USTC settlement and appeals procedures and strategies. Moreover, a notice of assessment may be appealed through the Commission’s appeals process. Accordingly, the taxpayer must file the appeal within 30 days of the date of the notice or the assessment becomes final.

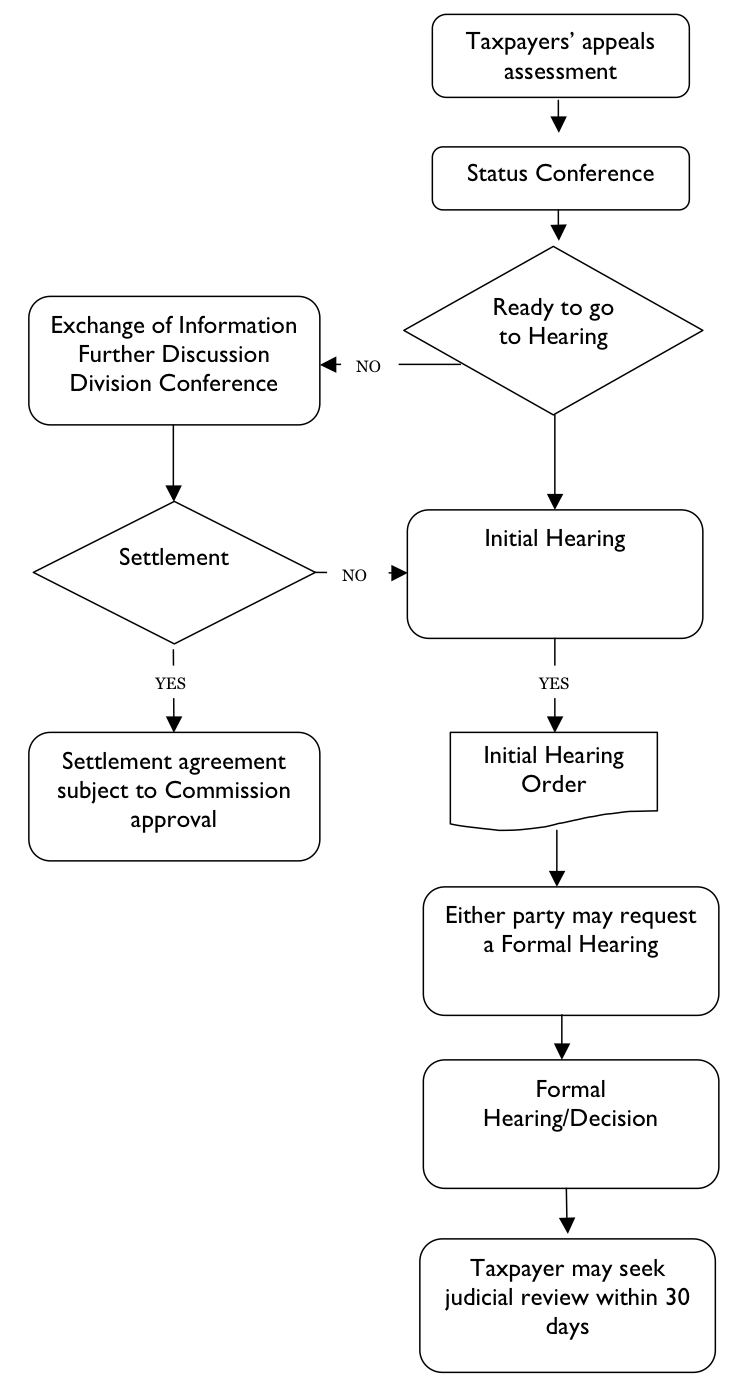

In our experience, most of the disputes arising from income tax audit assessments are resolved through interaction or negotiation between parties. Therefore, most of these appeals are routinely scheduled for a telephone status conference with an Administrative Law Judge, who screens the case, helps to defines the issues, and allows the parties additional time to work toward a resolution, if appropriate.

If the parties reach agreement, the Commission will issue an order approving the agreement or accepting a withdrawal of the appeal. On the other hand, if this process does not result in a settlement, the matter proceeds to a hearing.

If you receive a USTC Notice of Determination indicating that you owe additional taxes or fees, take careful note of the issue date. You have 30 days from the date of the notice of determination to file an appeal. Also, you file can request an appeal by filing a petition for redetermination. Consequently, if you do not pay the proposed tax liability or file an appeal by the 30-day deadline, you will be assessed a penalty equal to ten percent of the unpaid taxes or fees due. Furthermore, there are several steps involved in the appeals process. In some cases, an appeal can be referred back to a prior step. Thus, you may go through some of the steps in the appeals process more than once.

USTC Settlement

After you file your petition for redetermination, your case can go to the settlement division. In the settlement division, the settlement officer typically will review your arguments for why and how the auditor made mistakes at arriving the proposed tax assessment. The settlement officer will review your arguments and any documentation you have provided. After reviewing the matter, the USTC settlement officer will propose a percentage reduction to the proposed liability. If you accepted this proposal, you generally must pay a 25% down payment toward the tax assessment and then pay the remaining amount within two years.

USTC Appeals

If you ask to skip the settlement process or fail to reach an agreement with the settlement division, you appeal will be referred back to the appeals division. Eventually an appeals officer will review your case, including your arguments and any documents provided to substantiate your position. An appeals officer has a wider degree of authority to settle issues and can even remove entire portions or all of the assessment. If you fail to reach an agreement with the appeals officer, your case will be transferred back to settlement.

You must appeal in writing, within 30 days of the date on the notice of the action that you are challenging. However, although your appeal need not be in any particular form, the following links are provided to assist you.

What to Include

Your appeal should contain the following information:

- Your name, address, and daytime telephone number;

- The tax type involved, the time period and the amount of tax, penalty, interest, or other issue in dispute;

- The agency’s file or other reference number, if known, and a copy of the letter or document which you are appealing;

- The name, address, and daytime telephone number of your representative, if any.

Contact an USTC Tax Attorney

If you have received a notice from the USTC, contact an USTC tax attorney at Tax Defense Counsel for a free consultation.